7 Best Savings Challenge Envelopes For Older Kids

Help your children master money management with our list of the 7 best savings challenge envelopes for older kids. Shop our top picks and start saving today!

Managing a childs allowance or earnings from neighborhood jobs often starts with a simple piggy bank, but that system rarely survives the transition to middle school. As children take on more complex financial responsibilitieslike saving for a high-end gaming console, a musical instrument upgrade, or club sports feesthey require tools that mirror the structure of real-world budgeting. Transitioning to an envelope system provides the tactile feedback necessary to transform abstract money concepts into concrete progress.

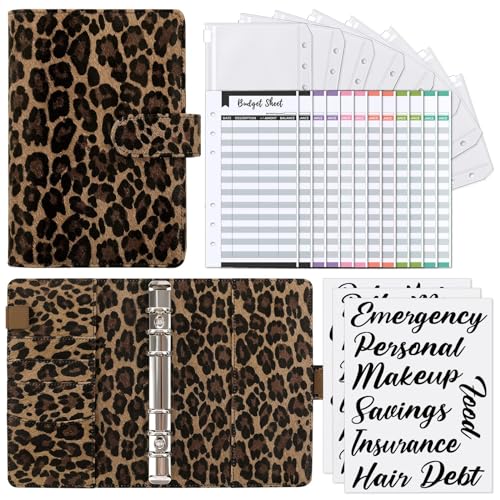

Antner A6 Binder: Best All-In-One Financial Starter

As an Amazon Associate, we earn from qualifying purchases. Thank you!

For the twelve-year-old just beginning to manage their own extracurricular funds, complexity is often the enemy of consistency. The Antner A6 binder serves as an entry-level command center, housing cash, ledger sheets, and goal trackers in one compact, portable unit. It is an ideal bridge for the pre-teen who needs to separate money for soccer cleats from funds allocated for weekly outings.

This binder’s modular design accommodates the reality of shifting adolescent interests. If a child decides to pivot from one hobby to another, the internal pockets can be reorganized or swapped without needing a brand-new system. It is a cost-effective, durable starting point that teaches the fundamental habit of categorized saving.

Soligt Laminated Envelopes: Most Durable for Daily Use

Active, extracurricular-heavy kids are often hard on their gear, and a flimsy paper envelope will not survive a season of being tossed into a gym bag or locker. Soligts laminated envelopes provide the necessary reinforcement for daily handling and frequent retrieval. They hold up under the pressure of constant use, ensuring that “saving for later” does not become “losing the cash today.”

These envelopes are best suited for children aged ten and up who have reached a level of commitment where they are physically managing their own activity fees. Because they are designed for longevity, they represent a solid investment that can survive several school years. The laminated surface also allows for repeated marking with dry-erase pens, making them perfect for children who like to update their totals daily.

Savvyfox 100 Envelope Kit: Perfect for Big Goal Tasks

Some financial goalslike saving for a summer intensive workshop or a specialized piece of art equipmentrequire a structured, long-term roadmap. The Savvyfox 100 Envelope Kit excels here by gamifying the process, turning the daunting task of accumulating a large sum into smaller, bite-sized milestones. It is particularly effective for the child who needs a visual dopamine hit to stay motivated over several months.

Using this system helps a child break down a large, intimidating goal into manageable tasks. It creates a psychological win each time an envelope is filled, which is a powerful developmental reinforcement for perseverance. It is best used for specific, high-cost objectives rather than general weekly allowance management.

Clever Fox Cash Envelopes: Best for Long-Term Planning

Consistency is a difficult skill for younger adolescents to master, especially when the reward for saving is delayed by several months. Clever Fox envelopes are designed with a clean, professional aesthetic that appeals to older teens who have outgrown “kiddie” banking solutions. Their structure encourages a more mature approach to budgeting, such as separating “saving,” “spending,” and “donating.”

These envelopes provide the space to log transactions directly on the surface, which reinforces the habit of tracking every dollar in or out. For the child who is starting to earn significant money through babysitting or yard work, this system fosters a sense of financial autonomy. It is the gold standard for teaching teens the difference between impulse buying and strategic allocation.

BetterDay Horizontal Envelopes: Best Visual Trackers

For the child who is a visual learner, abstract numbers on a screen often fail to convey the reality of financial progress. BetterDay horizontal envelopes feature built-in, easy-to-read progress bars that allow the child to color in their success as they save. This simple design choice makes the abstract concept of “growth” visible and tangible.

These work exceptionally well for younger teens aged 11 to 13 who are still learning to visualize the passage of time in relation to their goals. Seeing the progress bar fill up provides a sense of agency that digital statements simply cannot replicate. It turns a standard budgeting chore into an engaging visual project.

Skycase A6 Money Organizer: Top Choice for Busy Teens

The teenager involved in multiple activitiesfrom band practice to after-school jobsneeds an organization system that is as mobile as they are. The Skycase A6 organizer is compact, secure, and fits easily into a backpack or school bag. Its zippered closure ensures that no cash or receipts are lost during the chaos of a busy school day.

This is a functional choice for the student who requires a high level of efficiency. It respects the fact that a busy teen does not have time for overly complicated systems, focusing instead on rapid access and secure storage. It is an excellent choice for keeping activity-related expenses separated from personal leisure money.

Luckisix Clear Envelopes: Best for Visible Milestones

Transparency is a powerful motivator for children who struggle to remember how much they have saved. The Luckisix clear envelopes allow the child to see their physical cash hoard growing, providing an immediate, undeniable indicator of their hard work. For a child who has been working toward a goal for months, the sight of a full, thick envelope is highly gratifying.

These are best used for short-to-medium-term goals where constant visual reinforcement is necessary to keep the child on track. Because the contents are always visible, they also serve as a constant reminder of the child’s financial commitments. Use these for children who need that extra nudge to avoid dipping into their savings for small, unnecessary treats.

Moving Beyond Pigs: Why Older Kids Need System Tools

Traditional piggy banks are designed for the accumulation of coins, not the management of a budget. As kids enter their middle school years, their financial lives include diverse income streams and specific, high-cost expenses. Moving to an envelope system shifts the child’s mindset from “storing” money to “managing” it.

This transition mimics the adult reality of allocating funds to different buckets: rent, utilities, and savings. When a child learns to partition their resources, they develop a sense of ownership over their choices. It moves them from a passive saver to an active financial planner.

How Savings Challenges Build Delayed Gratification Skills

The ability to delay gratification is a significant predictor of future success, and physical savings challenges are the perfect training ground for this skill. By using a visual tracker, a child learns that todays sacrifice leads to a much larger, more satisfying reward in the future. This is the exact same discipline required to master a musical instrument or train for a varsity sport.

These systems teach that progress is rarely linear and often requires sustained effort. When a child encounters a setback or a dip in their savings rate, the envelope system allows them to see exactly where the disconnect occurred. This develops resilience and the capacity for self-correctionskills that are infinitely more valuable than the money inside the envelopes.

Balancing Digital Apps and Physical Cash Management

While digital banking apps are common, they strip away the sensory experience of handling money, which is crucial for brain development in early adolescence. Physical cash forces the child to think twice before spending; the act of removing a bill from a designated envelope is much more psychologically “painful” than a digital swipe. This friction is a feature, not a bug, of cash-based systems.

For the best results, use physical envelopes for “spending” categories like snacks or small hobbies, while reserving digital accounts for long-term savings. This hybrid approach teaches the child that different types of money require different levels of interaction and care. It creates a well-rounded financial education that prepares them for both the physical and digital realities of adulthood.

Helping a child move from passive saving to active financial management is one of the most practical investments a parent can make. By choosing a system that matches their current maturity level, you provide them with the autonomy and structure they need to succeed in their future endeavors.